ASEAN's Logistics Boom: How Vietnam and Indonesia Are Becoming the New Manufacturing Supply Chain Hubs

The China Plus One strategy is no longer a contingency plan — it's the default playbook for global manufacturers in 2026. As tariff pressures intensify and geopolitical uncertainty persists, Vietnam and Indonesia have emerged as the most compelling alternatives for companies diversifying their production footprint. But building factories is the easy part. The real question is whether Southeast Asia's logistics infrastructure can keep pace with its manufacturing ambitions.

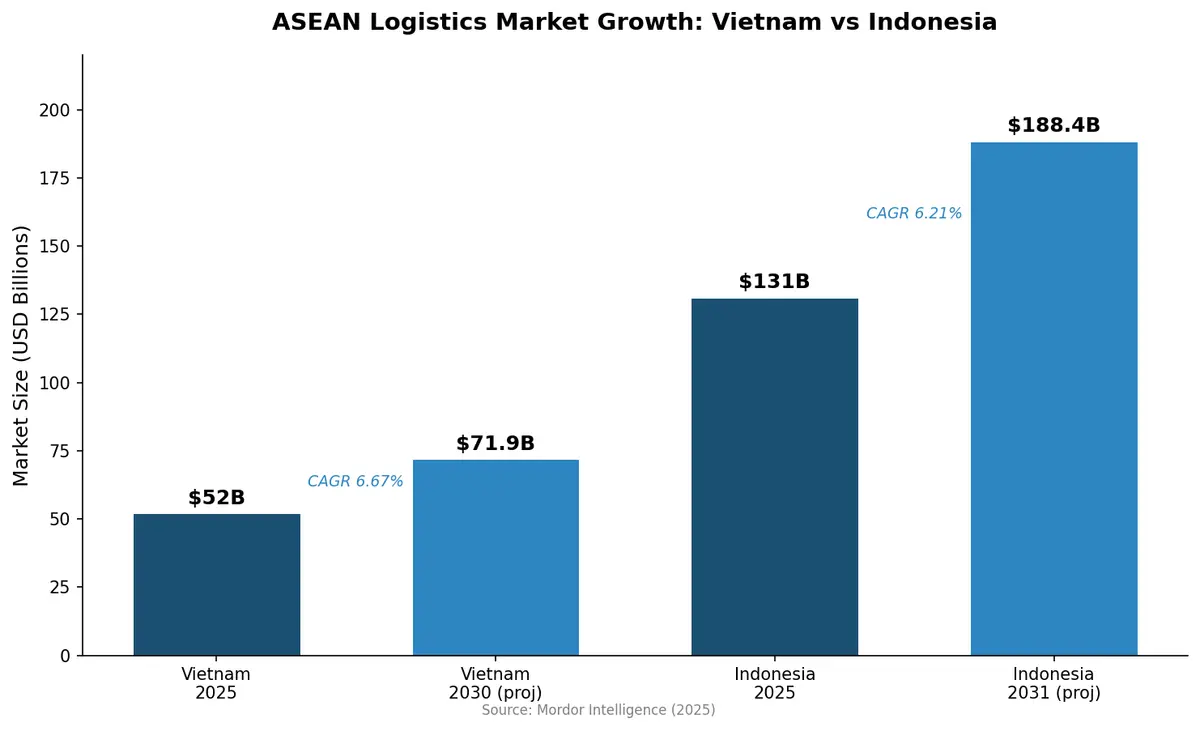

Vietnam's $52 Billion Logistics Engine

Vietnam's freight and logistics market reached an estimated USD 52 billion in 2025 and is projected to grow at a 6.67% CAGR to reach $71.9 billion by 2030, according to Mordor Intelligence. That trajectory reflects more than a decade of deliberate infrastructure investment now reaching critical mass.

The centerpiece is Long Thanh International Airport, a $16 billion mega-project outside Ho Chi Minh City targeting commercial operations by June 2026. Phase 1 will handle 25 million passengers and significant air cargo volume, providing southern Vietnam with a world-class logistics gateway that the overcrowded Tan Son Nhat airport can no longer support. Combined with the new Long Thanh–Ho Chi Minh City expressway, the project creates an integrated air-road corridor purpose-built for export manufacturing.

Vietnam's deep-water port capacity is expanding in parallel. The Cai Mep–Thi Vai port complex in Ba Ria-Vung Tau province already handles ultra-large container vessels on direct routes to North America and Europe, while the planned Phuoc An port in Dong Nai province will add capacity closer to industrial zones in the southern economic corridor.

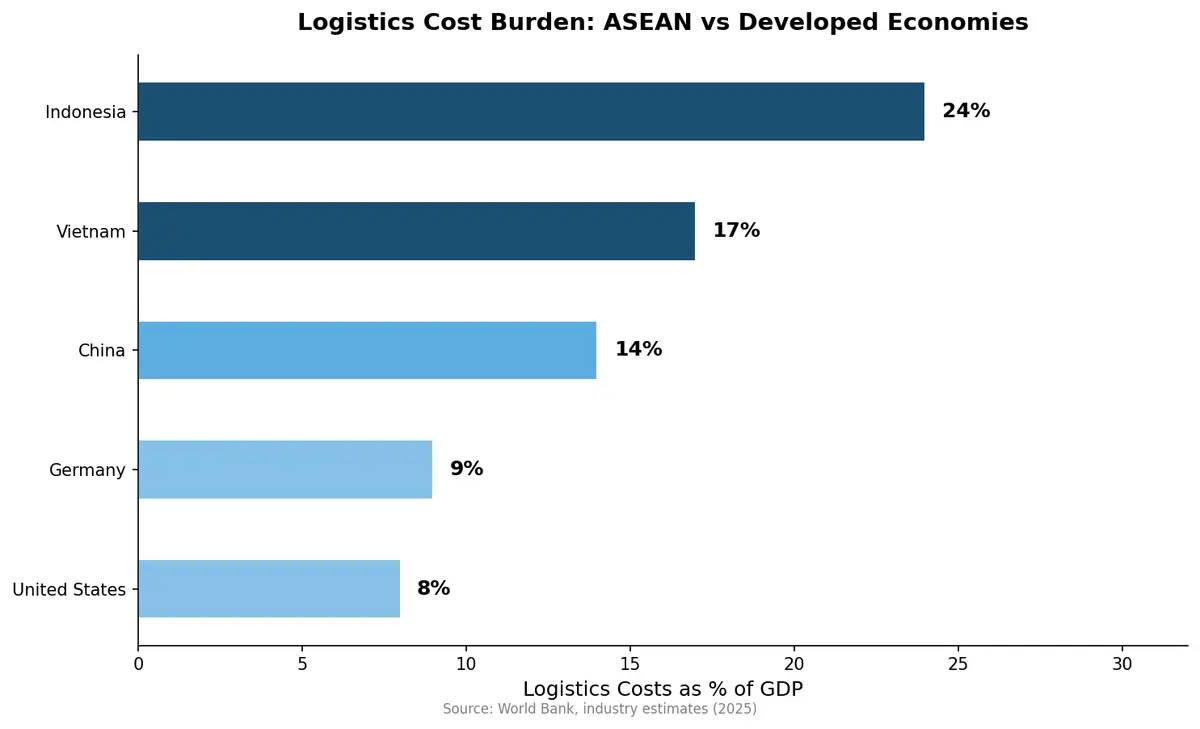

These investments address Vietnam's core logistics challenge: despite ranking as a top-15 global exporter of electronics and textiles, the country's logistics costs still consume an estimated 16–18% of GDP — nearly double the rate of developed economies.

Indonesia: Scale That Demands Attention

While Vietnam captures headlines for electronics manufacturing, Indonesia's logistics story is one of sheer scale. The country's freight and logistics market was valued at approximately USD 131 billion in 2025, growing at a 6.21% CAGR toward $188 billion by 2031, per Mordor Intelligence. As the world's fourth most populous nation and ASEAN's largest economy, Indonesia offers a domestic consumer market that most manufacturing hubs cannot match.

President Prabowo's administration has doubled down on the Indonesia Industrial Downstreaming agenda, requiring raw material processing (nickel, copper, bauxite) to occur domestically before export. This policy is driving a wave of smelter and battery manufacturing investment that creates entirely new freight corridors — particularly for EV supply chain components destined for global automakers.

The challenge for Indonesia remains its archipelagic geography. Moving goods across 17,000 islands requires sophisticated multi-modal logistics coordination. The government's ongoing investment in trans-Java toll roads, the Makassar New Port, and interisland shipping modernization are narrowing the infrastructure gap, but logistics costs remain high at an estimated 23–25% of GDP.

The China Plus One Accelerator

The shift toward ASEAN manufacturing has accelerated sharply since 2023. U.S. tariffs on Chinese goods — now exceeding 145% on many categories — have made the math undeniable. Companies that once viewed Southeast Asian production as a hedge are now treating it as their primary strategy.

Vietnam has been the biggest beneficiary. Foreign direct investment (FDI) in Vietnamese manufacturing hit record levels in 2024–2025, led by electronics giants Samsung, Apple suppliers like Foxconn and Luxshare, and semiconductor packaging firms. Samsung alone operates factories employing over 100,000 workers in northern Vietnam, producing roughly half of the company's global smartphone output.

Indonesia is attracting a different but equally strategic investment profile. Chinese EV battery makers CATL and nickel processors have invested billions in Sulawesi and Kalimantan, while Japanese automakers Toyota and Honda are expanding production capacity on Java to serve both domestic and export markets.

The ASEAN region collectively attracted over $230 billion in FDI in 2024, with manufacturing accounting for an increasingly dominant share.

Logistics Challenges That Still Need Solving

Despite the boom, ASEAN logistics remains fragmented and complex:

- Customs heterogeneity: Each ASEAN nation maintains distinct customs procedures, documentation requirements, and regulatory frameworks despite the ASEAN Economic Community's harmonization efforts

- Last-mile infrastructure gaps: Outside major industrial zones, road quality and intermodal connectivity deteriorate significantly

- Digital maturity variance: While Vietnam and Singapore are adopting digital customs platforms, Cambodia, Laos, and Myanmar lag substantially behind

- Cold chain limitations: Temperature-controlled logistics capacity remains underdeveloped across most of Southeast Asia, constraining food and pharmaceutical supply chains

- Port congestion: Key facilities like Laem Chabang (Thailand) and Cat Lai (Vietnam) regularly experience vessel queuing during peak seasons

For shippers establishing ASEAN trade lanes, these challenges mean that route optimization, carrier selection, and customs compliance cannot rely on the standardized playbooks that work in mature markets.

How Multi-Modal TMS Platforms Enable ASEAN Trade Lane Management

Managing freight across ASEAN's diverse logistics landscape requires technology that handles complexity by design. Modern transportation management systems are adapting to serve this market with capabilities including:

- Multi-country customs integration that maps documentation requirements across origin, transit, and destination countries within ASEAN

- Multi-modal optimization that evaluates ocean, air, road, and rail combinations across fragmented infrastructure networks

- Real-time carrier performance tracking across markets where reliability data has historically been sparse

- Currency and language localization for operations spanning multiple ASEAN markets simultaneously

- Tariff and trade agreement modeling that calculates landed costs under RCEP, ASEAN FTA, and bilateral trade agreements

The companies winning in ASEAN logistics are those that invest in visibility and orchestration technology early — before the complexity of managing 3–5 country manufacturing networks overwhelms manual processes.

The Strategic Imperative

ASEAN's logistics boom isn't a temporary shift. It represents a structural realignment of global manufacturing that will define trade patterns for decades. Vietnam and Indonesia sit at the center of this transformation, each offering distinct advantages: Vietnam for electronics, textiles, and light manufacturing speed; Indonesia for raw material processing, automotive, and domestic market scale.

For logistics leaders, the message is clear: the time to build ASEAN supply chain capabilities is now — while infrastructure is scaling up and competitive advantages are still available for early movers.

Expanding into Southeast Asian trade lanes? Contact CXTMS to see how our multi-modal TMS platform simplifies ASEAN logistics management.